Il PIL come parametro indicatore dell’andamento reale del mercato immobiliare

GDP as a yardstick for the real estate market

- 14 Gen 2018

Nell’ambito del mercato immobiliare, quello che in generale si evidenzia è la continua presenza sui canali di informazione di notizie discordanti tra segnali di chiara ripresa e crisi continua. Quindi l’utente medio si rassegna per lo più a “pensare ad altro” e ad effettuare investimenti immobiliari in base “alla sensazione dell’amico del momento” in quanto sistematicamente e, spesso, intenzionalmente, si trova confuso anche dal continuo contrasto tra informazioni di analisti seri ed altre generate “ad arte” dai servizi stampa per operazioni di marketing o di tipo lobbistico.

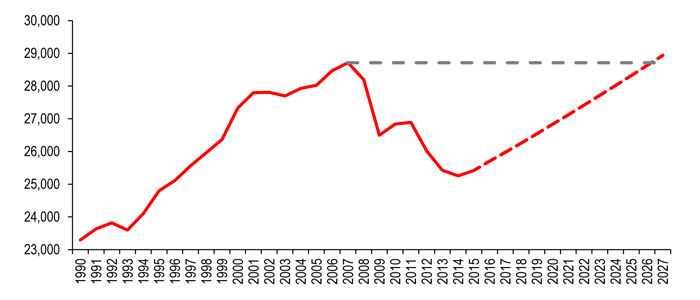

andamento PIL 1990-2016-2027 (elaborazione Confartigianato)

In realtà, al di là delle mille parole, dei rumors e del chiacchiericcio interessato degli speculatori, l’unico dato certo disponibile per un’analisi effettiva (e necessariamente a lungo termine) è che il mercato dell’immobile segue l’andamento della realtà economica reale di un paese e quindi del parametro PIL in un rapporto circa equivalente. Pertanto, a meno delle bolle speculative e delle mode create artificialmente nel tempo ed ormai a intervalli più o meno regolari (generalmente in corrispondenza dell’entrata in attività lavorativa delle nuove generazioni di popolazione attiva) in alternanza con quelle finanziarie per generare acquisizione/spostamento di denaro, l’andamento dei valori degli immobili, in crescita o in decrescita in realtà socio-economiche consolidate, segue i tempi dell’economia e quindi intervalli lunghi e, soprattutto, in relazione a situazioni di basso livello di crescita e di mancanza di prospettiva economica come quella italiana, sempre più dilatati.

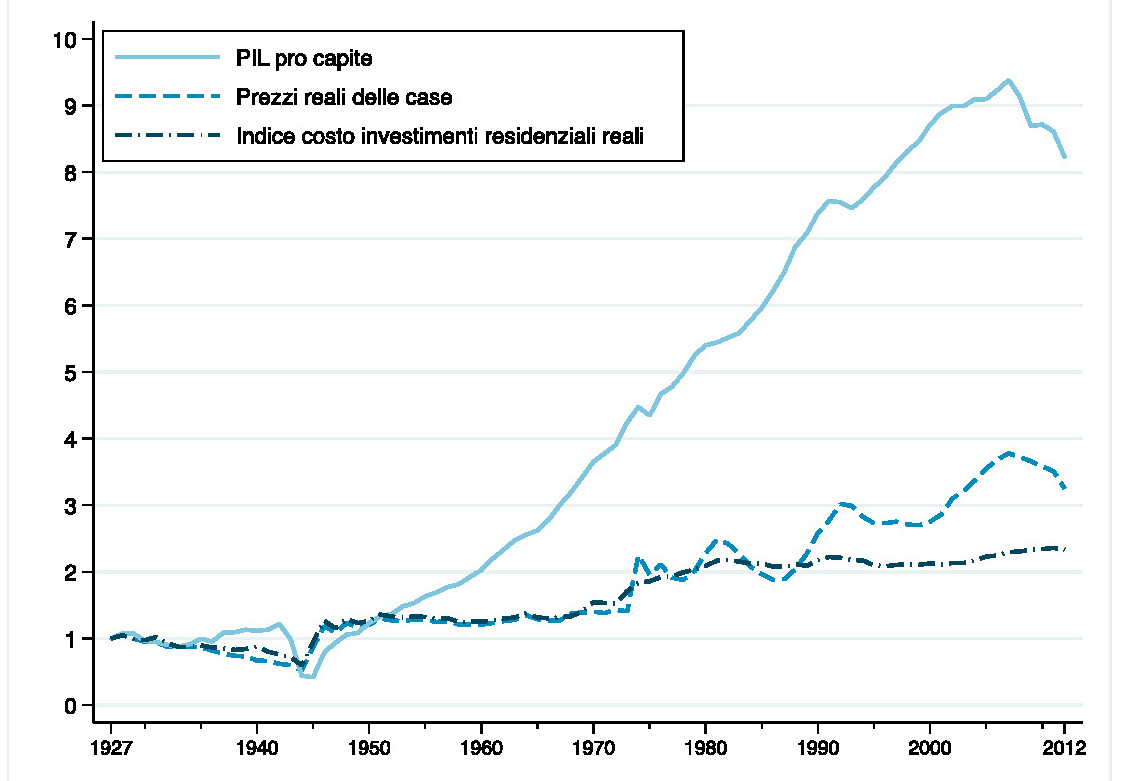

Con riferimento alle serie storiche dal 1927 al 2012 si osserva infatti che in Italia l’aumento della ricchezza in rapporto al PIL è stato considerevole a partire dalla metà degli anni sessanta del secolo scorso: per la ricchezza delle famiglie si è passati da un valore di circa 3 volte il PIL nel 1964 a un valore di circa 6 nel 2012. In modo associato, dalla metà degli anni sessanta i prezzi delle case sono significativamente aumentati in termini reali: posto pari a 1 il valore del 1964 i prezzi delle case avevano raggiunto il valore di 2,4 nel 2012. Come spunto di approfondimento si può considerare che in tale periodo l’aumento dei prezzi delle abitazioni è attribuibile in buona misura all’aumento del prezzo dei terreni fabbricabili. In genere, ed in particolare per tale periodo in Italia, la crescita del valore dei terreni fabbricabili è plausibilmente legata alle pressioni demografiche ed ai fenomeni di urbanizzazione, avvenuti in un territorio limitato e sottoposto a vincoli via via più stringenti. La crescita delle abitazioni in aree periferiche, meno pregiate e più lontane dal centro, hanno innalzato la richiesta (e dunque il valore) delle abitazioni preesistenti costruite nelle aree centrali, facendo emergere significativi capital gains. Se poi si estende l’analisi a livello internazionale, in Italia oltre due terzi dell’aumento del prezzo delle case intervenuto tra il 1950 e il 2012 è attribuibile alla variazione del prezzo dei terreni edificabili, questa quota è però inferiore a quanto si osserva in altre economie avanzate, segno che le pressioni sui prezzi delle aree fabbricabili nel nostro paese sono state comunque meno intense che in altre economie.

Si può inoltre osservare che l’incremento del PIL ha consentito un’ampia diffusione della quota di possesso delle abitazioni: già nel 1951 il 40% delle famiglie erano proprietarie dell’abitazione di residenza; nel 2012 (peraltro in pieno periodo recessivo) la quota di proprietari ha sfiorato l’80%.

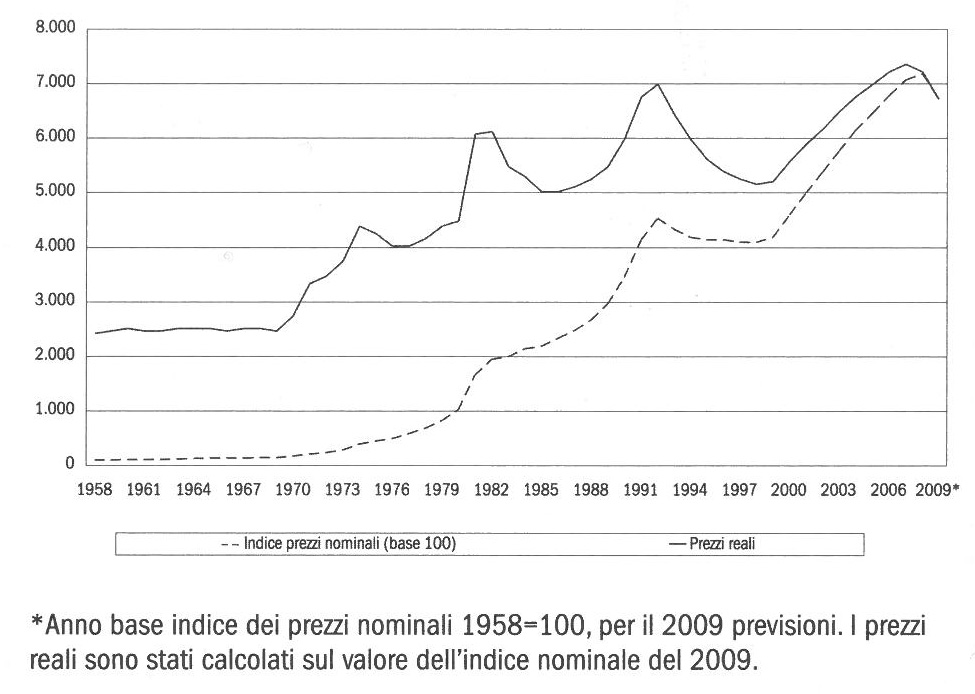

Un altro elemento da tenere in considerazione, osservando in modo ingrandito la curva dei valori reali, è che il mercato immobiliare è caratterizzato da cicli relativamente lunghi, con periodi di contrazione cui seguono periodi di rialzi dei prezzi. Le fasi di rialzo che durano diversi anni possono portare alcuni investitori a sottovalutare il rischio di un investimento immobiliare: per esempio, nel mercato residenziale alla fine degli anni Ottanta e nei primi anni Duemila ci sono stati lunghi periodi di crescita continua. Questo tipo di comportamento si rispecchia, per esempio, nella convinzione di molti investitori, prevalentemente privati, secondo cui il rendimento immediato di un immobile rappresenta il rendimento “base” per tale investimento, che sarà ulteriormente migliorato da una plusvalenza quasi sicura nel medio-lungo periodo. In realtà emerge chiaramente una ciclicità del mercato con periodi di elevata riduzione dei prezzi. L’investitore inesperto che percepisce un basso rischio si focalizza solo sulla curva dei prezzi nominali e spesso considera solamente due punti della stessa in cui registra dei valori certi (il momento di acquisto e il momento di vendita): in tal modo quindi difficilmente si osservano, erroneamente, i reali rendimenti negativi che si vengono a creare.

In modo corretto si deve invece considerare che i tempi di recupero del valore massimo a seguito di una fase di decrescita è attualmente dell’ordine di 20 anni con periodi di crescita, a partire dal valore di minimo raggiunto, di circa 10 anni ma con differenze tra i valori massimi acquisiti dall’immobile che tendono sempre più a ridursi nel tempo (anche in relazione alla vetustà ed ai nuovi standard abitativi che si stanno affermando a livello internazionale).

Altro elemento da valutare è che l’investitore medio, quale è una famiglia, effettua l’acquisto non necessariamente in fase di minimo ma in base al momento di disponibilità economica e non avrà certo un portafoglio immobiliare su cui diversificare per ridurre i diversi rischi connessi all’investimento (di mercato, ambientale, difetti dell’edificio, di liquidità, di gestione e finanziario) e quindi assume sempre fondamentale ed imprescindibile importanza effettuare un’analisi della qualità della costruzione, delle modifiche potenziali della location dell’immobile e dell’evoluzione possibile dell’area.

fonti:

“Questioni di Economia e Finanza (Occasional Papers) I prezzi delle abitazioni in Italia, 1927-2012” – Cannari, D’Alessio e Vecchi N. 333 giugno 2016 – Banca d’Italia

“Investimento immobilare” Hoesli, Morri – Ed. HOEPLI

https://www.confartigianato.it/

http://www.soldionline.it/

Ing. Luca Persia – ZED PROGETTI srl

In the real estate market, what is generally highlighted is the continuous presence on the information channels of news that differed between signs of a clear recovery and a continuing crisis, and the average user resigns himself to “think about something else” and to make real estate investments on the basis of “the feeling of the moment” as it is systematically and often, intentionally, confused also by the continuous contrast between information from serious analysts and other information generated by press services for marketing or lobbying operations.

In reality, the only sure element in a real (and necessarily long-term) analysis is that the property market follows the trend of a country’s real economic reality and thus of the GDP parameter in a roughly equivalent ratio.

Therefore, apart from the speculative bubbles and fashions artificially created over time and now at more or less regular intervals (generally in correspondence with the entry into employment of the new generations of active population) alternating with financial ones to generate acquisition / displacement of money from the masses, its trend, which is growing and decreasing in consolidated socio-economic realities follows long timescales and, above all, in relation to situations of low level of growth and lack of economic perspective such as that one.

In fact, with reference to the historical series from 1927 to 2012, it can be seen that in Italy the increase in wealth as a ratio to GDP has been considerable since the mid-sixties of the last century: for the wealth of families it has increased from a value of about 3 times the GDP in 1964 to a value of about 6 in 2012. In associated terms, house prices have significantly increased in real terms since the mid-sixties: house prices reached 2.4 in real terms by 1 in 1964, compared to 2.4 in 2012. As a basis for further analysis, it can be considered that the rise in house prices during this period is to a large extent attributable to the increase in the price of buildable land. In general, and in particular for this period in Italy, the growth in the value of land that can be built is plausibly linked to demographic pressures and urbanization, which have occurred in a limited territory and are subject to increasingly stringent constraints. The growth of housing in peripheral areas, less valuable and further away from the centre, has raised the demand (and therefore the value) of existing dwellings built in central areas, leading to the emergence of significant capital gains. If the international analysis is extended, in Italy more than two thirds of the increase in house prices between 1950 and 2012 is attributable to the change in the price of building land, this share is however lower than that observed in other advanced economies, a sign that pressure on the prices of manufacturable land in our country was however less intense than in other economies.

It can also be observed that the increase in GDP has allowed a wide diffusion of the share of home ownership: already in 1951,40% of households owned the residence; in 2012 (in the middle of a recessionary period) the share of owners has reached almost 80%.

Another element to be taken into account when looking at the real value curve in an enlarged way is that the real estate market is characterised by relatively long cycles, with periods of contraction followed by periods of price increases. The upward phases that last several years may lead some investors to underestimate the risk of a real estate investment: for example, in the residential market at the end of the 1980s and in the early 2000s there were long periods of continuous growth. This type of behaviour is reflected, for example, in the belief of many investors, mainly private investors, that the immediate return on a property represents the “basic” return on that investment, which will be further improved by an almost secure capital gain in the medium to long term. In fact, there is a clear evidence of cyclicality in the market with periods of high price reductions. The inexperienced investor who perceives a low risk focuses only on the nominal price curve and often only considers two points of the same where he records certain values (the moment of purchase and the time of sale): in this way negative returns are hardly observed, wrongly. Instead, it must be considered that the maximum value recovery times following a phase of decrease are currently in the order of 20 years with periods of growth, starting from the minimum value reached, of about 10 years but with differences between the maximum values acquired by the property that tend to decrease more and more over time (also in relation to the value of the property).

Another element to be evaluated is that the average investor, such as a family, does not necessarily make the purchase in phase of minimum but on the basis of the moment of economic availability and will certainly not have a real estate portfolio on which to diversify in order to reduce the different risks connected with the investment (market, environmental, building defects, liquidity, management and financial) and therefore it assumes a fundamental and essential importance to always carry out an analysis of the quality of the construction, of the potential changes in the location of the property.