IMPIANTI FOTOVOLTAICI E CATASTO

PHOTOVOLTAIC PLANTS AND LAND REGISTER

- 14 Mag 2023

Le considerazioni che seguono riguardano gli impianti di produzione di energia elettrica da fonte fotovoltaica in merito all’eventuale censimento in catasto degli stessi.

Si vogliono dapprima richiamare, in termini generali, le motivazioni che furono alla base dell’istituzione in Italia del catasto urbano, che più ci interessa nell’ambito della presente analisi. A tale fine, occorre fare riferimento a:

- Regio Decreto Legge 13/04/1939 n. 652, nel quale:

- si legge (art. 1) <<È disposta …omissis… l’esecuzione a cura dello Stato dell’accertamento generale dei fabbricati e delle altre costruzioni stabili non censite al Catasto rustico, allo scopo di:

1) accertare le proprietà immobiliari urbane e determinarne la rendita;

2) costituire un catasto generale dei fabbricati e degli altri immobili urbani che si denomina nuovo Catasto edilizio urbano …omissis…>>;

- viene data la seguente definizione di immobili urbani (art. 4): <<Si considerano come immobili urbani i fabbricati e le costruzioni stabili di qualunque materiale costituite, diversi dai fabbricati rurali. Sono considerati come costruzioni stabili anche gli edifici sospesi o galleggianti, stabilmente assicurati al suolo>>.

- L. 31/03/2005 n. 44, nel quale (art. 1-quinquies) si legge che <<…omissis… l’articolo 4 del regio decreto-legge 13 aprile 1939, n. 652, convertito, con modificazioni, dalla legge 11 agosto 1939, n. 1249, limitatamente alle centrali elettriche, si interpreta nel senso che i fabbricati e le costruzioni stabili sono costituiti dal suolo e dalle parti ad esso strutturalmente connesse, anche in via transitoria, cui possono accedere, mediante qualsiasi mezzo di unione, parti mobili allo scopo di realizzare un unico bene complesso. Pertanto, concorrono alla determinazione della rendita catastale, ai sensi dell’articolo 10 del citato regio decreto-legge, gli elementi costitutivi degli opifici e degli altri immobili costruiti per le speciali esigenze dell’attività industriale di cui al periodo precedente anche se fisicamente non incorporati al suolo …omissis…>>.

Da quanto precede, risulta che, <<limitatamente alle centrali elettriche>>, la rendita catatale di un immobile di tale tipologia deve tenere conto di elementi costitutivi compresi nello stesso, anche se <<non incorporati al suolo>>, quale può essere, ad esempio, un impianto fotovoltaico installato sulla copertura dell’immobile.

La questione è stata successivamente oggetto di attenzione da parte dell’Agenzia delle Entrate, che, dal 1° dicembre 2012, ha incorporato l’Agenzia del Territorio, quest’ultima competente in materia catastale. Di specifico interesse è la Circolare del 19/12/2013 n. 36/E – Agenzia delle Entrate “Impianti fotovoltaici – Profili catastali e aspetti fiscali”, nella quale si legge quanto segue:

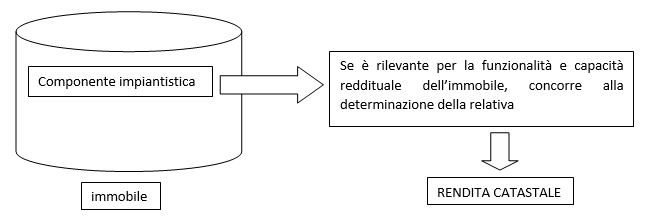

- (punto 1.1) <<…omissis… ai fini dell’obbligo di accatastamento e della determinazione della rendita catastale di un impianto fotovoltaico, non è fondamentale esclusivamente la facile amovibilità delle sue varie componenti impiantistiche, quanto, piuttosto, il rapporto di tali componenti con la capacità ordinaria dell’unità immobiliare a cui appartengono di produrre un reddito temporalmente rilevante. In altri termini, gli Uffici Provinciali – Territorio dell’Agenzia accertano gli immobili che ospitano i medesimi impianti, indagando, ai fini della determinazione della relativa rendita catastale, sulla correlazione che sussiste tra l’immobile e, in generale, quelle componenti impiantistiche rilevanti ai fini della sua funzionalità e capacità reddituale, a prescindere dal mezzo di unione utilizzato.

…omissis…

Tale concetto è stato ulteriormente ribadito, in termini più generali, nella sentenza della Corte Costituzionale n. 162 del 20 maggio 2008, ove si stabilisce che “(… tutte quelle componenti […] che contribuiscono in via ordinaria ad assicurare, ad una unità immobiliare, una specifica autonomia funzionale e reddituale stabile nel tempo, sono da considerare elementi idonei a descrivere l’unità stessa ed influenti rispetto alla quantificazione della relativa rendita catastale)”>>.

Si può schematizzare quanto sopra riportato nella figura che segue.

fig.1

(punto 1.1) <<L’Agenzia del Territorio ha quindi definito …omissis.. criteri in applicazione dei quali è stata affermata l’irrilevanza catastale delle installazioni fotovoltaiche non con esclusivo riferimento all’amovibilità delle stesse, ma in relazione da un lato all’alea propria delle stime catastali e dall’altro alla loro modesta entità in termini dimensionali e di potenza, in coerenza con i criteri, concettualmente analoghi, di cui all’art. 3, comma 3, del citato decreto ministeriale n. 28 del 1998, che indica, in linea generale, le costruzioni prive di rilevanza catastale>>.

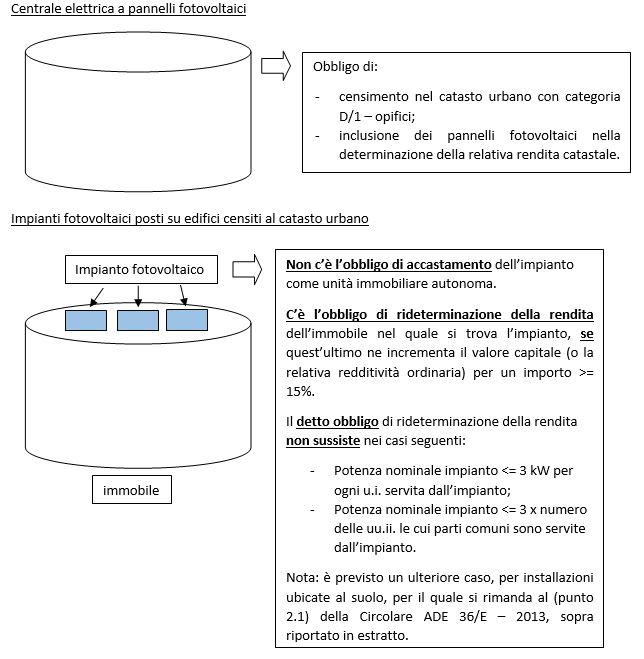

- (punto 2.1) <<In linea generale, coerentemente con quanto precisato nella risoluzione n. 3/T del 6 novembre 2008, si ribadisce che gli immobili ospitanti le centrali elettriche a pannelli fotovoltaici devono essere accertati nella categoria “D/1 – opifici”>>, o “D/10 – fabbricati per funzioni produttive connesse alle attività agricole” qualora abbiano i requisiti di ruralità, << e che nella determinazione della relativa rendita catastale devono essere inclusi i pannelli fotovoltaici, in quanto ne determinano il carattere sostanziale di centrale elettrica e, quindi, di “opificio”.

Con riferimento alle installazioni fotovoltaiche poste su edifici ed a quelle realizzate su aree di pertinenza, comuni o esclusive, di fabbricati o unità immobiliari censiti al catasto edilizio urbano, si precisa che, in coerenza con i principi generali esposti nella citata risoluzione n. 3/T del 2008, non sussiste l’obbligo di accatastamento come unità immobiliari autonome, in quanto possono assimilarsi agli impianti di pertinenza degli immobili. In proposito, si chiarisce che è necessario procedere, con dichiarazione di variazione da parte del soggetto interessato, alla rideterminazione della rendita dell’unità immobiliare a cui risulta integrato, allorquando l’impianto fotovoltaico ne incrementa il valore capitale (o la relativa redditività ordinaria) di una percentuale pari al 15% o superiore, in accordo alla prassi estimativa adottata dall’amministrazione catastale. In tal senso, erano state fornite istruzioni con circolare n. 10/T del 4 agosto 2005, nell’ambito dell’applicazione dell’art. 1, comma 336, della legge 30 dicembre 2004, n. 311.

… omissis…

non sussiste alcun obbligo di dichiarazione al catasto, né come unità immobiliare autonoma, né come variazione della stessa (in considerazione della limitata incidenza reddituale dell’impianto) qualora sia soddisfatto almeno uno dei seguenti requisiti:

- la potenza nominale dell’impianto fotovoltaico non è superiore a 3 chilowatt per ogni unità immobiliare servita dall’impianto stesso;

- la potenza nominale complessiva, espressa in chilowatt, non è superiore a tre volte il numero delle unità immobiliari le cui parti comuni sono servite dall’impianto, indipendentemente dalla circostanza che sia installato al suolo oppure sia architettonicamente o parzialmente integrato ad immobili già censiti al catasto edilizio urbano;

- per le installazioni ubicate al suolo, il volume individuato dall’intera area destinata all’intervento (comprensiva, quindi, degli spazi liberi che dividono i pannelli fotovoltaici) e dall’altezza relativa all’asse orizzontale mediano dei pannelli stessi, è inferiore a 150 m3, in coerenza con il limite volumetrico stabilito dall’art. 3, comma 3, lettera e) del decreto ministeriale 2 gennaio 1998, n. 28>>.

Si ritiene utile effettuare una sintesi schematica di quanto riportato nei riferimenti normativi sopra elencati, distinguendo il caso delle centrali elettriche dalle altre situazioni di interesse.

fig.2

Si aggiunge che, ancora nella sopraccitata Circolare ADE 36/E – 2013, al punto 2.1 dell’Allegato, si legge quanto segue:

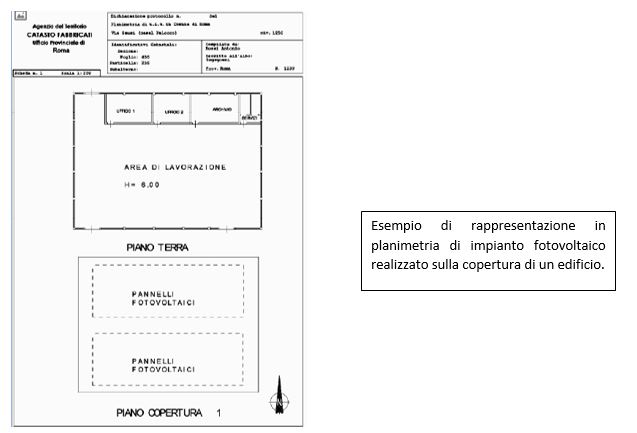

<<Con riferimento alle installazioni fotovoltaiche architettonicamente integrate o parzialmente integrate … omissis… le installazioni fotovoltaiche realizzate sulla copertura si indicano con linea tratteggiata, come nell’esempio di seguito riportato>>.

fig.3

Quale ultimo elemento della Circolare ADE 36/E – 2013, si richiama quanto previsto in merito ad immobili ospitanti le centrali elettriche a pannelli fotovoltaici e censiti nel catasto urbano con la categoria “D/10 – fabbricati per funzioni produttive connesse alle attività agricole”. Si osserva unicamente che, affinchè si abbia tale inquadramento catastale, è necessario che i detti immobili abbiano i requisiti di ruralità, descritti, in sintesi, nel punto 2.2 della suddetta Circolare, non oggetto delle presenti considerazioni.

Si vuole, in conclusione, in relazione alle possibili sinergie tra impianti fotovoltaici ed attività agricole, fare un cenno ad un argomento di più recente interesse: i sistemi agrivoltaici. Trattasi di sistemi nei quali si persegue un duplice obiettivo, produzione agricola e produzione energetica fotovoltaica, quali risultanti da due sottosistemi organizzati in una struttura integrata. Di particolare interesse è il cosiddetto sistema agrivoltaico avanzato, nel quale i moduli fotovoltaici sono installati sospesi da terra ed opportunamente distanziati tra di loro, in maniera che ci sia molto spazio lasciato libero alle coltivazioni; quindi buona parte del suolo è lasciata a disposizione delle colture, mentre la porzione residua è utilizzata per le strutture di sostegno dell’impianto fotovoltaico. I sistemi agrivoltaici sono stati recentemente (aprile 2023) oggetto di un interessante provvedimento normativo, vale a dire la proposta di decreto agrivoltaico PNRR (Piano Nazionale di Ripresa e Resilienza), firmata dal Ministro dell’Ambiente e della Sicurezza Energetica, Gilberto Pichetto Fratin, trasmessa alla Commissione Europea per il relativo esame al fine dell’approvazione.

Con l’obiettivo di installare almeno 1,04 GW di impianti agrivoltaici entro il 30 giugno 2026, saranno in particolare favorite soluzioni costruttive di nuova concezione, prevalentemente a struttura verticale e con moduli ad alta efficienza, ed è previsto il riconoscimento di un incentivo costituito da un contributo in conto capitale nella misura massima del 40% dei costi ammissibili e da una tariffa incentivante relativa alla quota di energia elettrica prodotta e immessa in rete. L’intera procedura sarà curata dal Gestore Servizi Energetici (GSE).

Fonti:

- Bollettino di Legislazione Tecnica 3.2023 marzo

- EdilTecnico – Il quotidiano online per professionisti tecnici

Ing. Fabio Di Matteo – ZED PROGETTI srl

Ing. Fabio Di Matteo – ZED PROGETTI srl

The following considerations concern photovoltaic power generation plants with regard to their possible census in the cadastre.

First of all, we would like to recall, in general terms, the motivations behind the institution in Italy of the urban cadastre, which is of most interest to us in this analysis. To this end, reference should be made to:

– Royal Decree Law n. 652 of 13/04/1939, in which:

o it reads (art. 1) <<It is provided …omissis… the execution by the State of the general assessment of buildings and other stable constructions not registered in the rustic cadastre, in order to:

1) ascertain urban real estate and determine its income;

2) constitute a general land register of buildings and other urban immovable property which is called the new Urban Land Register …omissis…>>;

o the following definition of urban real estate is given (Article 4): <<Buildings and stable constructions made of whatever material, other than rural buildings, are considered as urban real estate. Also considered as stable constructions are suspended or floating buildings, stably secured to the ground>>.

– Decree-Law no. 44 of 31/03/2005, in which (art. 1-quinquies) it is stated that <<…omissis… Article 4 of Royal Decree-Law no. 652 of 13 April 1939, converted, with amendments, by Law no. 1249, limited to power stations, is to be interpreted in the sense that buildings and permanent constructions are constituted by the land and the parts structurally connected to it, even temporarily, to which movable parts may be attached by any means of union in order to create a single complex asset. Therefore, the constituent elements of factories and other buildings constructed for the special needs of the industrial activity referred to in the preceding sentence, even if they are not physically incorporated to the ground, contribute to the determination of the cadastral income, pursuant to Article 10 of the cited Royal Decree-Law, even if they are not physically incorporated to the ground …omissis…>>.

From the foregoing, it follows that, <<limited to power stations>>, the catatal income of a property of this type must take into account constituent elements included in the same, even if <<not incorporated in the ground>>, such as, for example, a photovoltaic system installed on the roof of the property.

The issue has subsequently been the subject of attention by the Agenzia delle Entrate, which, as of 1 December 2012, incorporated the Agenzia del Territorio, the latter being responsible for cadastral matters. Of specific interest is the Circular of 19/12/2013 no. 36/E – Agenzia delle Entrate “Photovoltaic systems – Cadastral profiles and tax aspects”, which states the following:

– (point 1.1) <<…omissis… for the purposes of the obligation to register and determine the cadastral income of a photovoltaic system, it is not only fundamental the easy removability of its various plant components, but, rather, the relationship of such components with the ordinary capacity of the real estate unit to which they belong to produce a temporally relevant income. In other words, the Provincial Offices – Land Registry of the Agency ascertain the properties that house the same installations, investigating, for the purposes of determining the relative cadastral income, the correlation that exists between the property and, in general, those plant components relevant to its functionality and income capacity, regardless of the means of union used.

…omissis…

This concept was further reiterated, in more general terms, in the Constitutional Court’s sentence no. 162 of 20 May 2008, where it is stated that “(… all those components […] that ordinarily contribute to ensuring, to a real estate unit, a specific functional and income autonomy stable over time, are to be considered elements capable of describing the unit itself and influential with respect to the quantification of its cadastral income)”>>.

The above can be schematised in the figure1.(point 1.1) <<The “Agenzia del Territorio” has therefore defined …omissis… criteria in the application of which the cadastral irrelevance of photovoltaic installations has been affirmed, not with exclusive reference to their removability, but in relation, on the one hand, to the uncertainty inherent in cadastral estimates and, on the other, to their modest entity in terms of size and power, in coherence with the criteria, conceptually analogous, set forth in art. 3, paragraph 3, of the aforementioned Ministerial Decree No 28 of 1998, which indicates, as a general rule, buildings without cadastral relevance>>.

– (point 2.1) <<As a general rule, in line with what has been set forth in Resolution No. 3/T of 6 November 2008, it is reiterated that buildings hosting photovoltaic panel power plants must be ascertained in the category “D/1 – factories”>>, or “D/10 – buildings for productive functions related to agricultural activities” if they meet the requirements of rurality, << and that photovoltaic panels must be included in the determination of the relevant cadastral income, as they determine their substantial character of power plant and, therefore, of “factory”.

With reference to photovoltaic installations placed on buildings and to those realised on areas of appurtenance, common or exclusive, of buildings or real estate units registered in the urban building cadastre, it is clarified that, consistently with the general principles set forth in the above mentioned resolution No. 3/T of 2008, there is no obligation to register them as autonomous real estate units, as they can be assimilated to installations pertaining to buildings. In this regard, it is clarified that it is necessary to proceed, with a declaration of variation by the party concerned, to recalculate the income of the real estate unit to which it is integrated, when the photovoltaic system increases its capital value (or its ordinary income) by a percentage equal to 15% or more, in accordance with the estimative practice adopted by the cadastral administration. Instructions to this effect were provided in Circular no. 10/T of 4 August 2005, in the context of the application of Article 1, paragraph 336 of Law no. 311 of 30 December 2004.

… omissis…

… there is no obligation to file a declaration with the Land Registry, either as an independent property unit or as a variation thereof (in consideration of the limited income impact of the system) if at least one of the following requirements is met

o the nominal power of the photovoltaic system is no more than 3 kilowatts for each property unit served by the system

o the total nominal power, expressed in kilowatts, is no more than three times the number of the building units whose common parts are served by the system, regardless of whether it is installed on the ground or is architecturally or partially integrated with buildings already registered in the urban building cadastre

o for ground-mounted installations, the volume identified by the entire area destined for the intervention (thus including the free spaces dividing the photovoltaic panels) and by the height relative to the horizontal median axis of the panels themselves, is less than 150 m3, in accordance with the volumetric limit established by Article 3, paragraph 3, letter e) of Ministerial Decree no. 28 of 2 January 1998>>.

It is deemed useful to provide a schematic summary of the regulatory references listed above, distinguishing the case of power plants from other situations of interest.

Photovoltaic panel power plant. See fig. 2It should be added that, again in the above-mentioned Circular ADE 36/E – 2013, at point 2.1 of the Annex, the following is stated

<<With reference to architecturally integrated or partially integrated photovoltaic installations … omissis … photovoltaic installations made on the roof are indicated with a dotted line, as in the example below>>. See fig. 3

As a final element of ADE Circular 36/E – 2013, reference is made to what is provided for in respect of buildings hosting photovoltaic panel power plants and registered in the urban cadastre with the category ‘D/10 – buildings for productive functions related to agricultural activities’. It is only noted that, in order to have such cadastral classification, it is necessary that the said buildings meet the requirements of rurality, described, in brief, in point 2.2 of the above Circular, which is not the subject of the present considerations.

In conclusion, in relation to the possible synergies between photovoltaic systems and agricultural activities, we would like to mention a topic of more recent interest: agri-voltaic systems. These are systems in which a dual objective is pursued, agricultural production and photovoltaic energy production, as the result of two subsystems organised in an integrated structure. Of particular interest is the so-called advanced agri-voltaic system, in which the photovoltaic modules are installed suspended from the ground and suitably spaced so that there is plenty of space left free for cultivation; thus a large part of the soil is left available for cultivation, while the remaining portion is used for the supporting structures of the photovoltaic system. Agri-voltaic systems have recently (April 2023) been the subject of an interesting piece of legislation, namely the PNRR (National Recovery and Resilience Plan) agri-voltaic decree proposal, signed by the Minister for the Environment and Energy Security, Gilberto Pichetto Fratin, and forwarded to the European Commission for consideration for approval.

With the goal of installing at least 1.04 GW of agri-voltaic plants by 30 June 2026, new-concept construction solutions will be particularly favoured, mainly with a vertical structure and high-efficiency modules, and an incentive will be recognised consisting of a capital contribution of up to 40% of eligible costs and an incentive tariff related to the share of electricity produced and fed into the grid. The entire procedure will be handled by the “Gestore Servizi Energetici” (GSE).